")

Sustainable Investing In Volatile Times: Key Takeaways from CNA Money Mind TV Episode with STACS

Money is pouring into ESG funds – where priority is given not just to financial performance, but also environmental, social and governance factors of a company.

Can the trend for sustainability continue in this volatile economic environment?

That’s what a July episode of CNA’s Money Mind television episode explored with a range of guests including STACS’ Co-founder & Managing Director Benjamin Soh; James Cheo, Chief Investment Officer, Southeast Asia at HSBC Global Private Banking and Wealth; Dale Hardcastle, Partner at Bain & Company.

Financial institutions are gearing up to meet the ESG challenge, by ensuring staff have the expertise to guide new investors.

Choosing the right companies can be tricky due to the lack of high-quality data that is used to assess a company’s ESG credentials.

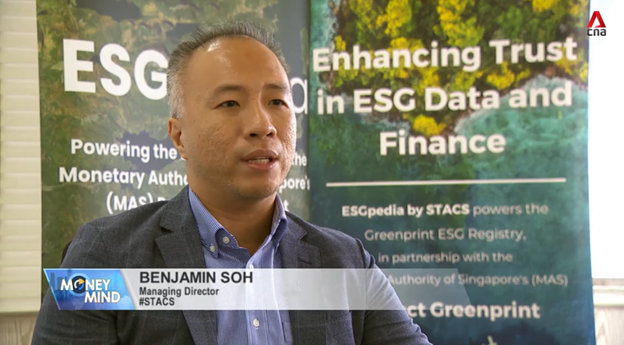

Developed in partnership with the Monetary Authority of Singapore’s (MAS) Project Greenprint, ESGpedia by STACS is a registry that aggregates data such as ESG certification and carbon credits, providing a one-stop shop for investors and financial institutions to have better oversight of their investments.

One of the challenges facing the sector is the perception that investors need to sacrifice returns if they want to include ESG factors in their portfolio, especially when oil and gas is enjoying a resurgence in the stock market.

Shares of the world’s biggest energy majors have outperformed every other sector since the start of Russia’s invasion of Ukraine – shares of Exxon are up more than 40 per cent since the start of year while the S&P 500 is down (as of July).

Proponents, however, say this is just transitory: in the seven years leading up to the pandemic, studies showed that the top third of companies ranked by ESG ratings outperformed the bottom third by more than 2.5 per cent each year.

It’s early days yet, but experts say that companies paying attention to ESG factors are more likely to be resilient and therefore better positioned to weather future uncertain conditions.

Some key statistics that the episode highlighted to provide context include:

- It’s estimated that by 2025, ESG investments will reach US$53 trillion, according to Bloomberg, which is a third of global assets under management. For now, it’s mainly the sphere of institutional investors but retail investors are also coming on board.

- 80 per cent of investors want to make ESG central to their investing strategy, according to HSCB. Sectors that are attractive in Southeast Asia include renewable energy, particularly solar and wind.

Key snippets from each contributor in the episode are paraphrased below:

James Cheo, Chief Investment Officer, Southeast Asia at HSBC Global Private Banking and Wealth

James Cheo, Chief Investment Officer, Southeast Asia at HSBC Global Private Banking and Wealth

In such a complex and difficult time, using ESG as a lens for investment is going to become much more important.

Companies that embrace and do well on ESG have strong leadership and higher productivity from employees.

Also importantly, they are less likely to breach environmental issues and as a result are better able to adapt to this very complex environment and will likely do better than those that don’t.

ESG investing is not that complicated – at the heart of it it’s really a spectrum: on one end you want to exclude companies that might not aligned with your values such as tobacco or weapons, while on the other hand you want to include companies that score well on ESG factors and long-term thematics such as the energy transition.

In terms of risk management, it’s clear that companies that score highly on ESG do better on a risk management basis because they are less prone to reputation risk associated with environmental breaches or labour rights issues.

On performance, if you stretch things out over the long term the difference is clear – you see companies with stronger ESG practices outperform in terms of financial matrixes from earnings to profitability.

If you look just at share price on a short-term day to day basis, the difference is harder to tell so you have to take a step back and look at it through a longer term lens.

Dale Hardcastle, Partner at Bain & Company

Dale Hardcastle, Partner at Bain & Company

Our estimates are that US$15 billion of new dedicated investment from non-governmental sources has been committed since the end of 2020, and over half of that in the last three quarters.

That cuts across many different sectors of the economy – corporates have been the largest investors with about 80 per cent of that, which has been primarily going into the renewables as well as the mobility sector.

In some ways, ESG investing went through a golden first chapter with a convergence of factors lining up to make it very attractive, some of which was fundamentals around the early stage of building many of these new industries.

A decade of extremely low energy prices meant many other sectors that might traditionally have competed for capital have been very poor investments.

Suddenly we’re moving into a new phase with the unfortunate events in Ukraine, rising inflation in petroleum and food prices, which is creating a comparison between the relative returns in one sustainable asset class versus the old economy that is having somewhat of a resurgence in terms of equity share prices and returns.

There are more difficult choices now for investors, particularly ESG managers, around how they balance the two.

Benjamin Soh, Co-founder & Managing Director, STACS

Benjamin Soh, Co-founder & Managing Director, STACS

ESG disclosed today are largely historical self-disclosures done once a year with no independent ongoing data that reflects how a company is doing on an ongoing basis, which means investors are not able to manage the risks of their portfolio on a real-time basis.

Besides that, data usually comes only from the larger companies so there’s a lot of missing data gaps in the supply chain or portfolio of any company.

A lot of ESG data is non-digital and in various parts of the industry that is not captured by the financial sector today, but the good news is that a lot of it is already available.

We’ve been able to aggregate this data from traditional industry platforms such as fleet management providers in the logistics sector, building management systems, and plantation/factory facilities in manufacturing and agriculture.

We’re able to connect all this data directly to our registry and provide an ongoing view of any company’s ESG performance.

On top of self-disclosures, we also partner and integrate Internet of Things (IoT) platforms and remote sensing technology directly at source so companies have no way to make up the data they send us.

PRESS CONTACTS

If you are a journalist with media queries, contact us.